Stablecoin Series Part 1 — Terra UST

by tiny hand

This perhaps might be the most “outrageous” stablecoin till date, but also a cryptocurrency that would bring great impact to the real world.

We would not be able to fully understand Terra’s operating logic if we view Terra UST simply as another type of cryptocurrency or another public chain. Terra’s competitors were never other public chains but real world payment instruments. When we view Terra and its stablecoins as a game-changer, everything would make sense.

Beginnings

“Cryptocurrencies for Payment”

Terra’s team also acknowledged that Alipay was their benchmark when they started creating a cryptocurrency payment system. As compared to Alipay, Terra faces further challenges, which is to break down the wall between the “real world” and the “crypto world”.

First Wall — Stable and Reliable Settlement Medium

Unlike Alipay which uses fiat currency/ legal tender for settlement, most cryptocurrencies fluctuate and are unable to ensure stability in its purchasing power. Terra needs to design a stablecoin that is suitable for itself as it lacks a stable currency it could rely on for settlement. I believe that in the initial discussions, the Terra team would have had fierce debates over which stablecoin to adopt. They contemplated if centralised stablecoins that rely on traditional financial assets as reserves, such as USDT be adopted, or a new stablecoin which better suits decentralisation and rely on crypto assets as collateral, be created. Terra ultimately went with the latter and introduced algorithmic mechanisms to create UST — a new algorithmic stablecoin.

Introduction of UST and LUNA

Pegged to USD, UST is a type of cryptocurrency that leverages algorithmic mechanisms to maintain stability. As of 3rd March 2022, there was over US$13.2 billion UST in circulation, becoming the algorithmic stablecoin with the greatest market value.

LUNA mainly serves as — (1) a price stability mechanism, (2) ecosystem collateral and governance as well as (3) the issuance of stablecoins.

These 2 types of token are interchangeable. For example, a user can destroy $1 USD worth of LUNA to create 1 UST, or destroy 1 UST to exchange for LUNA worth $1 USD.

Stability is fundamental to stablecoins. So how does UST maintain stability?

1.Arbitrage

When there is an excessive low demand for UST, the price of stablecoins will be lower than fiat currency/ legal tender.

Assuming the current market price of 1 UST is $0.9 USD, the arbitrage process would be as follows:

(1)Take $0.9 USD to buy 1 UST

(2)Take 1 UST to exchange for Luna worth $1 USD

(3)Sell Luna worth $1 USD and get $1 USD

In this process, 1 UST will be destroyed to create Luna worth $1 USD. The destruction of UST would lead to a reduction in the supply of UST, causing the market price of UST to rise. When the price of UST is near $1 USD, arbitrage opportunities disappear, and the price of UST could be pegged to USD again.

When there is an excessive demand for UST, the price of stablecoins will be higher than fiat currency/ legal tender.

Assuming the current market price of 1 UST is $1.1 USD, the arbitrage process would be as follows:

(1)Take $1 USD to buy Luna

(2)Take Luna worth $1 USD to exchange for 1 UST

(3)Sell 1 UST on the market to get $1.1 USD

In this process, Luna worth $1 USD will be destroyed to create 1 UST. As the demand for UST increases, the price of UST will fall. When the price is near USD 1, there would be no opportunity for arbitrage. The price of UST could then be pegged to USD.

2. Mining Incentive

Unlike most POS assets, the mining incentive for Luna is derived from the fees from each transaction on the chain, and not from inflation.

When transaction volume increases, cash flow and staker’s rewards would increase as well. This encourages more people to purchase LUNA. On the other hand, when transaction volume falls, cash flow generated from transaction fees will be reduced, resulting in a reduced demand for LUNA. Terra provides miners with stable, long term incentives through adjusting staking rewards, which reduces the volatility of mining incentives. This thereby increases UST’s stability as there is sufficient supply of LUNA for exchange.

UST achieved algorithmic stability through rewarding the “arbitrageurs” and “miners”.

Apart from algorithm design, another key to UST’s stability is use cases, which enables UST to be closer to fiat currency/ legal tender in nature. The concept that “mild inflation” is beneficial for economic development in traditional economics also applies to Terra’s ecosystem.

Second Wall — Real Application Scenarios

Algorithmic stablecoins in the market are largely used as liquid mining incentives. Once there is a reduction in high APY, or if there are comparable products with higher returns, holders will forsake them, which causes these stablecoins to be unhinged.

The common issue with this type of stablecoins is that it is unable to create use cases for itself, unlike UST. This is where Terra is smarter. Terra builds an ecosystem that surrounds UST, and constantly creates use cases to promote the demand for UST.

When the Terra chain was first introduced, there were no smart contracts. However, the team added a Cosmos module in order to construct an ecosystem surrounding UST. Subsequently, the team developed Mirror and Anchor, value adding Terra’s ecosystem.

Why are Use Cases Important to Stablecoins?

Use cases and capital are strongly interconnected; use cases are hyped up by capital, capital fills use cases. A cycle would be formed and when snowballed, the ecosystem and capital pool would increase. With a larger capital pool, the corresponding capital adequacy ratio would increase, reducing the risk of stablecoins being unhinged and hence making stablecoins safer.

Snowball Effect

Once there is money, there would not be a lack of reserves. If reserves are insufficient, just simply build another use case in other ecosystems!

Actually, Terra also does this. In the future, there will be a larger demand for stablecoins staking as multi-chain ecosystems are sprouting up while awaiting for ETH 2.0. Terra is capturing opportunities to deploy multi-chains and increase the liquidity of UST, by inserting UST into more ecosystems on other public chains and attempting to enable multi-chain staking assets to flow into Terra’s own ecosystem. With this, there will be more friends and the network of interconnected interests would expand, promoting market demand for UST.

Over the long term, the economy size of an open platform far exceeds that of a closed platform. Thus, constructing a diversified, large scale web would allow for more inflow and usage of funds, which I think is Terra’s greatest consideration when constructing its ecosystem at present.

Relevant Incidents

On 7 Jul 2021, Terra announced a $150 USD ecosystem fund, which will be used to sponsor projects that develop Terra’s ecosystem. This helps Terra reach the next development phase — strengthening accessibility for each ecosystem project, and achieve mainstream adoption.

On 10 Nov 2021, the proposal for Terra to destroy 886 million LUNA to create at least 3 billion UST was passed. Within several weeks, the total number of UST in circulation had increased significantly from $3 USD billion to $7 USD billion. This brought about sufficient imaginable space for the innovation of each of Terra’s DeFi agreements.

On 6 January 2022, Terra proposed to expand UST stablecoins’ cross deployment to Etherum, and 5 DeFi projects on Polygon and Solana (Olympus DAO, Rari Fuse, Invictus DAO, Convex, and Tokemak), thus supplying over US$139 million of UST and LUNA.

UST’s Usage based on Data and User

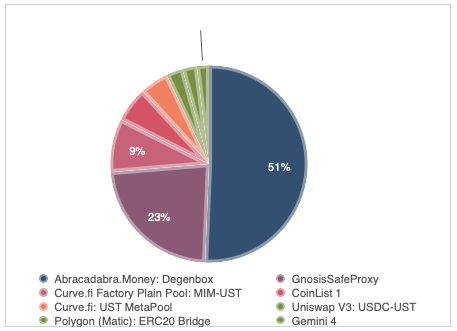

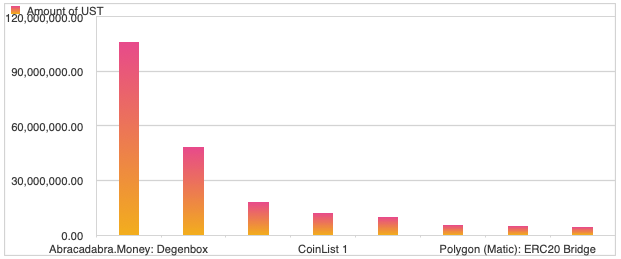

Top Wallet Addresses that Own UST:

Percentage of Top Addresses that Hold UST

Amount of UST held by Top Addresses

It is evident that the main uses of UST include DeFi lending and borrowing, asset management and stablecoin trading.

- Abracadabra Money, which ranks first, holds 105,973,077.95 UST, accounting for 33.15% of total UST. Abracadabra first uses interest bearing tokens for staking before creating original stablecoins to exchange and transact in UST, thereby creating huge demand for UST.

- Wonderland, DAO cross chain reserve currency agreement, which ranks second, holds large reserves of UST.

- Other main channels include — Agreements such as Curve that provide liquidity and form transaction pairs; acting as decentralised exchange and decentralised exchange reserves, etc.

Main Projects for UST Ecosystem

In 2021, the launch of Mirror protocol (Synths) and Anchor (lending/ borrowing) brought an enormous initial demand for UST.

LUNA’s Price Reflecting Market Demand (February to March 2022)

We could utilise the functions of various roles to compare projects which are more deeply connected to UST. For example, UST is equivalent to the Central Bank, Anchor is equivalent to banks and Mirror is equivalent to the financial market. Details are as follow:

1.Mirror Protocol(Financial Market)

Synths under Mirror are mainly created through UST, which makes it the most direct use case for UST. Users could stake excess amounts of UST stablecoins to compound real life assets, such as Alibaba, Tesla shares. Synthetic US equities created through staking are assets on the chain, which are allowed to be traded on DEX. Based on critical indicators like locked position transactions, transaction fee income, locked position, number of users, Mirror Finance has become the largest synthetic US equities blockchain exchange platform.

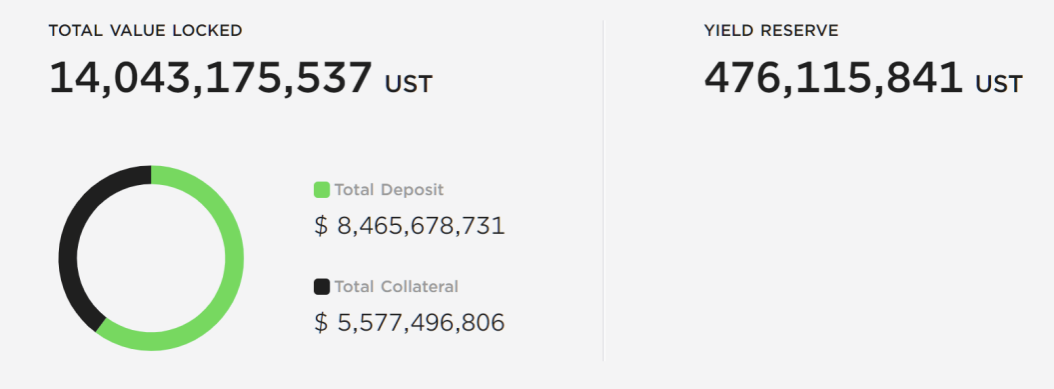

2.Anchor (Bank)

Anchor is a low risk, fixed yield financial instrument that only accepts original staking assets as collateral, and mainly attracts users with its fixed 20% annual yield. Anchor referenced UST from its pricing to its functions and has hedges up to 14 billion UST.

Total Value Locked and Corresponding Value

3.Other projects

There will be more projects in the future, which will be incorporated into Terra and are of relevance to UST.

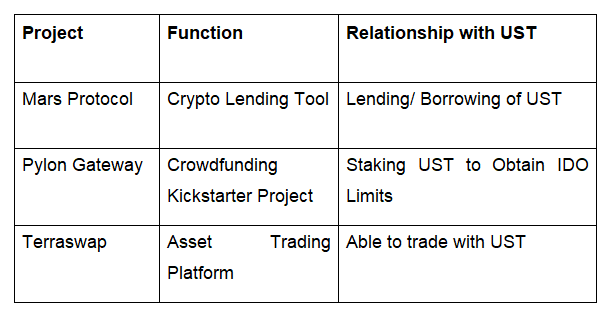

Mars Protocol, an open source credit protocol, uses UST for lending and borrowing. Pylon Gateway, a crowdfunding kickstarter project, stakes UST to obtain IDO limits. Terraswap, an asset trading platform on the chain, provides UST for trading with other assets.

In Terra’s ecosystem, numerous projects will have prerequisites for users to use “Terra stablecoins”, and distribute project tokens as rewards to these UST users. Currently, Terra’s ecosystem has expanded to payment, investment, lending and borrowing, savings, wallet, DEX transactions, NFT etc.

Third Wall — Combating the Real World

If we consider the two walls mentioned above to be Terra's own tech barriers in the crypto world, the third wall would be the barrier imposed by the real world. The barriers: 1) how do we make people receive UST payments in real life; and 2) how to create offline, real world payment use cases for online assets; would have to be addressed in the real world.

Take Terra's offline payment product, Chai, as an example. Chai became the payment app of choice for Korean businesses due to Terra’s collaboration with multiple Korean banks right from the beginning. Users could obtain partner merchant discounts or point rebates through their stablecoins spending on Chai. Although the stablecoins are mainly settled in KRW currently, it undoubtedly led people to look forward to using UST for offline payment.

Chai’s Official Website

However, using KRW for spending does not spell success for stablecoins. Afterall, currently only USD could represent the currency system as well as the benefits of old money of the old world. Once UST wishes to replace USD as a payment currency, there will be more issues to overcome.

In reality, Terra has broken norms, yet made use of norms, by choosing to interconnect with those that embrace cryptocurrencies. For example, Terra has chosen to build relationships with 15 companies which are main players in the e-commerce and O2O sector. This included Korea’s largest e-commerce company, TMON, and Korea’s largest travel platform, Yanolja. Terra has also connected itself with exchanges. Exchanges such as BINANCE LABS, OKX, Huobi and Dunamu appear on Terra’s investors list.

Subsequent Developments

In May 2021, SEC’s enforcement authorities issued a warrant to Do Kwon via email. Its contents were: investigations are underway on whether Terraform Labs and Do Kwon had breached Federal Securities Law, which included the sale of unregistered securities, as well as not being legally registered as an agent or dealer/ trader in the US, which references Terra’s Mirror agreement.

After this incident, people not only had concerns over the promotion and usage of UST. They also started to worry about decentralised stablecoins becoming unstable due to personal factors. Even if KRW is operating smoothly in Korea, however, once UST gets involved with US entities, UST would face greater pressure from regulations.

Community User Review

Conclusion

Terra’s UST has provided a new design mechanism for algorithmic stablecoins, proving that stablecoins could be an intermediary, which could also connect spending use cases on and off chain.

From the ecosystem distribution, we see that Terra’s ecosystem still mainly focuses on the DeFi area. With Web 3 creating new use cases and attracting more new users, for instance GameFi requires “gold hunting” and SocialFi requires rewarding, resulting in a greater demand for stablecoins capable of settlement. However, UST’s current ecosystem has yet to cover these areas. If competitors could come up with compatible products in these novel areas while Terra keeps to its strategy of “use cases dependent demand”, UST could soon be surpassed.

Web’s New Requirement Use Cases

Blockchain has now reached its second stage of development. Innovations such as NFT communities, GameFi and Web3 social networking have attracted new users and they wish to participate in it. At this stage, “connection” becomes the keyword. For example, infrastructure connection, offline data and online data connection, etc. In order for fiat currency/ legal tender to connect with cryptocurrencies, stablecoins would be essential. Similarly, each project that requires interaction and transfer of assets, would have to rely on stablecoins as well. In the future, for each project to have liberty, they will all have to issue their own stablecoins.