Recently, aside from the pandemic, another topic has dominated global financial headlines: interest rates.

Internationally, the Federal Reserve's unexpected rate cut on March 10 disrupted global financial market trends. Domestically, China has officially started transitioning existing loans to the Loan Prime Rate (LPR) policy.

The former marks the first unexpected rate cut since the 2008 financial crisis, while the latter affects people’s mortgages directly, impacting everyone's pocketbook.

This has sparked interest in and discussion about interest rates, reminiscent of the 2013 "money crunch" when many withdrew their savings from banks to deposit into higher-yielding money market funds like Yu'e Bao.

This article will start with the origins and definition of interest rates, explain the operational principles of various economic activities in commercial societies, and combine recent evolutions of interest rates in China to forecast future market directions—helping everyone gain a deeper understanding of interest rates.

We hope this sharing not only guides our investments and financial management but also enhances everyone’s understanding, stimulates independent thinking, reduces panic and excitement, and thus enables more accurate decisions.

Note that this article is primarily for public education. Since the author does not have experience working in major banks, big funds' fixed income departments, or academic economic research at universities, it will not cover interpretations of various interest rate products or analysis of trading methods.

01 The "Face" and "Core" of Interest Rates

Focusing on interest rate fluctuations and central bank rate adjustments is just the "face." Only by understanding the "core" of interest rates can we clarify how changes in the interest rate market affect the entire economy, thus improving market judgment accuracy and not getting lost in the noise of financial news and misinterpretations by self-media.

The author will unfold from these three questions, peeling back layers like an onion to analyze the essence of interest rates:

- Why do interest rates exist?

- What do high or low interest rates represent?

- How do interest rates explain all economic phenomena?

1. Why Do Interest Rates Exist?

Interest rates are one price of fiat currency; besides, there are exchange rates and prices.

Prices, known as the internal value of money, represent the commodity attribute of money, i.e., how much grain money can buy. Historically, before fiat currency, various objects such as precious metals like gold, silver, copper, and durable items like shells and stones were used as money.

The price of a country's currency compared to another's currency is the exchange rate, also known as the external value of money.

These two prices are similar to everyday transactions in markets and supermarkets, easily understood by the average person.

However, interest rates, known as the financial value or time value of money, though abstract and hard to grasp for the average person, are the cornerstone of all asset pricing.

Commercial activities related to interest rates, such as loans and bill discounting, appeared early among the public, but the combination and flourishing of these were driven by the issuance and circulation of government bonds.

In 1694, over a thousand shareholders raised 1.2 million pounds to invest in the Bank of England and lent the same amount to the government, receiving an equivalent amount of banknotes in return. Since this 1.2 million pounds was both the capital of the Bank of England and the shareholders' credit to the royal government, it amounted to the royal issuance of national debt through the Bank of England. This arrangement effectively allowed the Bank of England to act as a market maker for the circulation of government bonds. (Based on History of British Currency: The Birth and Unification of Banknotes)

The circulation of government bonds produced an asset reuse effect. The government borrowed 1.2 million pounds in gold coins, which circulated back into the public through military procurement, recruitment, and royal consumption. Although the wealthy had their money lent out, the government bonds could be used for discounting and converted into gold coins, leaving their businesses and investments unaffected.

This asset reuse was also reflected in subsequent municipal bonds, railway bonds, and stocks. From then on, the wealthy preferred to invest in and hold interest-bearing assets, securities, and deposits. A large amount of gold and banknotes flowed to workers, whose actual income increased, stimulating more trade and production, and factories and enterprises hired more people.

Therefore, modern financial operations involving cross-time calculations, such as the discounting of government bonds and securities, investment valuations, and loan matching, are all dependent on interest rates and connected by them.

After being transformed by modern finance, human society gradually realized that the essence of money is an incentive to organize production. Whether it is gold, silver, copper, or other objects is not important, as long as the money issued properly incentivizes production and innovation, severe inflation and severe depreciation are unlikely to occur, making the interest rate of fiat currency more important than the exchange rate and price.

2. What Do High or Low Interest Rates Represent?

For businesses, the level of interest rates means the cost of borrowing. Aside from the virtual economy such as the internet, the operation of real industries relies on inventory turnover, capital payment periods, and the tax benefits of long-term debt, which do not affect control rights, hence their short-term and long-term capital needs depend on borrowing and bond issuance.

For workers without fixed assets, the level of interest impacts the interest income from bank deposits and financial products. However, if high interest rates affect the normal operations of the real economy, causing businesses to scale back and workers to lose their jobs, the negative impact of reduced worker income will outweigh the benefits of increased financial interest income.

For workers with fixed assets, how interest rates affect asset price changes, especially stocks and residential properties familiar to the domestic audience, will be analyzed later in this article.

Here, some background knowledge is provided in advance to help better understand the role of interest rates in the economy:

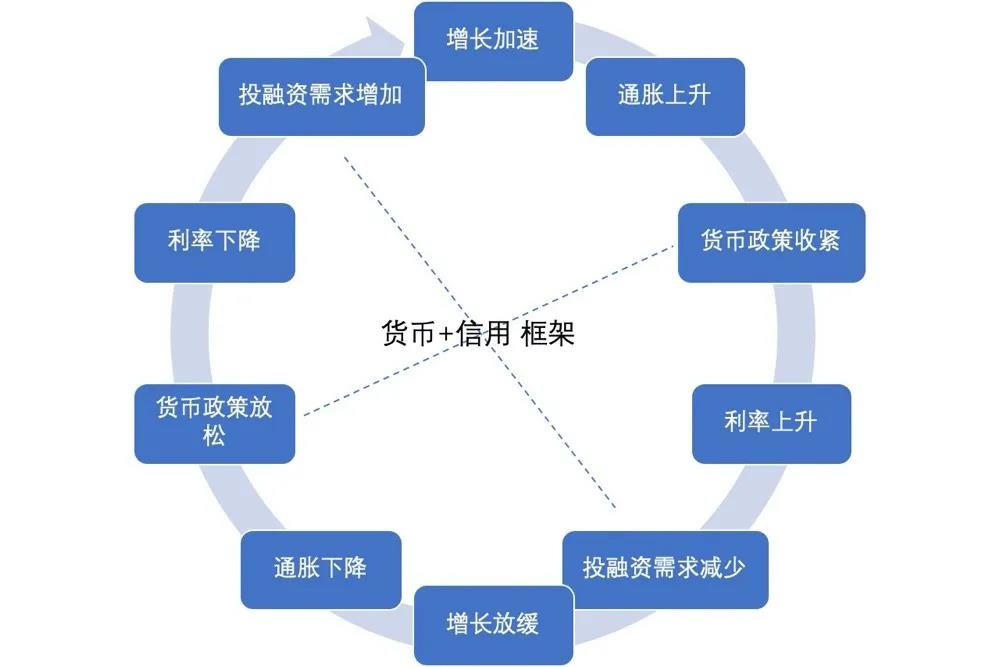

- Economic development necessarily supports the rise in corporate credit and investment financing, typically observed through data such as M2 and social financing growth.

- The government promotes the real and tangible use of newly borrowed money for production, known as credit easing. The central bank, as an independent department, adjusts interest rates to influence monetary tightness, with rate cuts known as easing or "loose money."

- Loose money, through certain transmissions, converts to credit easing. If the transmission is not smooth, it results in capital idling and shifting from real to virtual investments.

- Credit easing does not necessarily require loose money; it may also be prompted by technological advancements, deregulation, tax cuts, or foreign capital inflows.

3. Do Interest Rates Explain All Economic Phenomena?

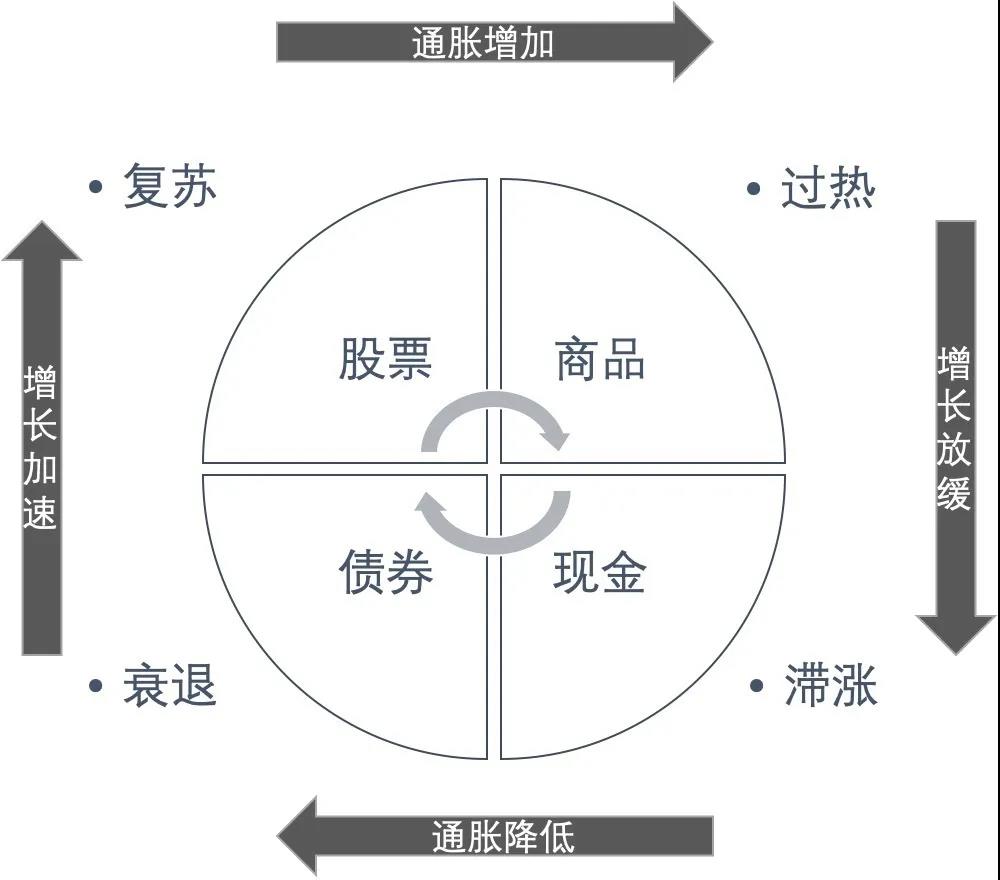

A commonly used theory that explains economic cycles and asset performance is the Merrill Clock.

The Merrill Clock uses economic indicators and inflation indicators to divide the economic cycle into: recession, recovery, overheating, and stagflation, corresponding to bonds, stocks, commodities, and cash as the appropriate investments for each phase.

However, the Merrill Clock is just an analytical indicator, a framework similar to a thermometer, it can only indicate the current market position and cannot predict turning points or divergences, making it not very useful for guiding actual investment actions.

But we can start with interest rates, deconstruct the Merrill Clock, and derive a clearer, more market-aligned logic.

Firstly, the signal that the economy is entering a recession is a decrease in corporate financing and investment, indicating tight credit. This leads to a decline in economic growth, income, demand, and consumption, followed by a decline in inflation, prompting the central bank to intervene by lowering interest rates, i.e., loose money. During this period, funds are mostly invested in bonds that benefit from falling interest rates.

Secondly, as interest rates decrease, it stimulates businesses to start borrowing, increasing capacity, and corporate financing and investment begin to rise, i.e., credit easing, and the economy begins to recover and rebound. During this period, funds are more invested in commodities benefiting from the recovery in financing and investment.

Thirdly, as the economy recovers, income increases, demand and consumption rise, leading to inflation, and the economy begins to overheat, prompting the central bank to intervene by raising interest rates, i.e., tight money. During this period, funds are more invested in stocks that benefit from inflation.

Lastly, as interest rates rise, although they have not yet impacted residents' income and consumption, inflation does not decrease, but corporate financing and investment begin to decline, indicating tight credit, economic growth stagnates, entering a stage of stagflation. During this period, funds adopt a "cash is king" strategy, entering the next cycle.

This analytical framework highlights how interest rates transmit to societal financing and investment, guiding corporate financing and production through changes in interest rates. Thus, this framework also has its moments of failure, particularly during significant international events affecting the global economy.

For example, the oil crisis and Vietnam War of the 1970s, due to the sudden increase in living and production costs and the post-war baby boom reaching adulthood, did not immediately lead to increased corporate efficiency despite significant investments in military and welfare expenditures in the United States. Although people cut back on expenses, their income did not improve, and the societal demand for goods only marginally decreased, failing to reduce inflation. This caused the central bank to hesitate in significantly lowering interest rates to avoid further stimulating inflation, while high interest rates led to some corporate bankruptcies and continued economic slowdown.

In that era, developed countries were caught in a long period of stagflation, eventually relying on technological advancements in the 1980s, Reagan's tax cuts, encouragement of privatization, and restructuring to increase social production and suppress inflation.

Another example occurred in the 1990s. At that time, the end of the Cold War, technological progress, and globalization expansion led the United States into a period of high economic growth and low inflation. Economically, this was reflected in increased corporate financing and investment, employment, and income, but because production increased faster, inflation did not rise significantly. Therefore, the central bank was able to maintain a policy of low interest rates. Low interest rates stimulated businesses to increase spending and production, further increasing people's income. This round of economic prosperity continued until the Asian financial crisis and the Russian debt crisis.

In conclusion, only technological progress and politics can break the rules of interest rates, but the rules of interest rates do not disappear; they are merely postponed.

Next, we will review China's situation over the past decade using interest rates.

02 Review of Interest Rates in China Over the Past 10 Years

Before 2008, the market was more concerned about the impact of CPI on interest rates, i.e., consumer-end inflation.

A significant component of CPI was pork prices. At the time, the pork industry was primarily based on scattered breeding, showing a trend of chasing highs and lows:

- When the economy improved, demand increased, pork prices rose, farmers increased pork production while also withholding pigs from the market to further drive up prices, pushing up CPI;

- Then the central bank would raise interest rates, reducing demand, and high pork prices also reduced market demand;

- Demand fell, pork prices plummeted, farmers hurriedly let pigs out of pens to minimize losses, but the increased supply of pork further drove prices down, causing CPI to fall.

- Once the central bank lowered interest rates, demand warmed up, starting a new cycle.

During this phase, CPI well reflected market demand fluctuations. Later, as pig farming gradually became more industrialized and professional, and as the economic situation changed, requiring central bank policies to align with the country's new growth models, CPI ceased to be a leading indicator for interest rate changes.

Before 2008, China also featured a growing disparity among regions. Coastal areas benefited from foreign capital and trade bonuses after joining the WTO, experiencing rapid development; some northern energy cities and political centers also enjoyed growth benefits; other regions developed slowly with simple economic activities, where most people primarily hoped for a better life. This confirmed that meat prices were the basic contradiction in the mainland at that time.

After the 2008 financial crisis, overseas orders and demand plummeted, and some foreign capital returned home to "put out fires." China needed to change the simple "China produces + the world consumes" model, and fiscal and monetary policies began to work together more to serve its own economic growth, namely the "four trillion" policy. On one hand, it was through infrastructure demand to integrate previously economically stagnant areas into the national market quickly; on the other hand, to meet the demand for infrastructure and future domestic growth, it lowered interest rates to support faltering and surplus industrial enterprises through difficulties and assist in their transformation.

During this phase, market factors influencing interest rates expanded from the past single focus on CPI to include nominal GDP, where nominal GDP equals economic growth + inflation. Industrial growth was the main contributor to economic growth during this phase, and industrial product inflation, namely PPI, accounted for most of the inflation. Therefore, it can also be said that the market believed that industrial growth rate + PPI influenced interest rates.

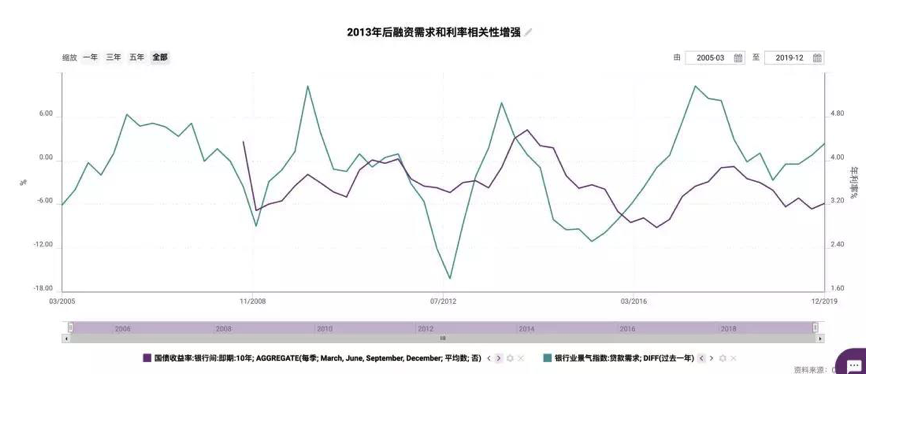

By 2013, the situation changed. On one side, industrial product prices, industrial growth rates, and nominal GDP growth rates were falling, but on the other side, interest rates were rising, and loan demand was increasing, leading to a divergence.

This phenomenon also occurred in 2017. When the signs first appeared, there were two viewpoints:

- One side believed that interest rates could not maintain high levels and would soon follow the economic growth rate's decline;

- The other side believed that the rapid response of capital to economic signals, with increased loans stimulating real production, would lead to an economic rebound and overheating.

As a result, in 2013, interest rates continued to rise. China even experienced two "money crunches," with all sectors borrowing money while economic growth did not improve significantly, and new loans did not lead to production. It wasn't until 2014 that both interest rates and economic growth rates fell.

Therefore, both viewpoints had flaws. Looking back, there was indeed a significant loan demand in 2013, but these loans were mainly used to repay debts and replenish cash. Once the debt issues were resolved, due to the economic downturn, there was no new loan demand, and interest rates began to decline.

Fundamentally, the economy from 2008 to 2012 was overly dependent on infrastructure and real estate. These sectors are highly sensitive to capital, involve one-time transactions, and are highly cyclical, causing a mismatch between upstream capital and downstream demand. The market has since stopped focusing on nominal GDP's impact on interest rates and shifted its focus to loan demand and social financing's impact on interest rates.

So, whether it was the early focus on CPI or the later focus on PPI + industrial growth rate, neither is as relevant today as focusing on loan demand and social financing. In the context of investment-driven economic growth in China, the willingness of businesses to actively seek loans, or credit conditions, has become the economic barometer and also drives interest rate changes. However, when businesses are no longer actively seeking loans and start cutting back, shutting down, or merging, the central bank may preemptively lower interest rates due to political awareness and the overall situation, easing this process or hoping businesses continue to expand.

This section outlined how factors affecting interest rates have evolved over time. Next, we will focus on the present and consider the future of interest rates and how they guide investment.

03 The Future of Interest Rates and Investment

For most people in China, the most accessible and reliable investment vehicles are residential properties, stocks, and bank financial products. The relationship between domestic stock prices and housing prices historically falls into two phases, with the turning point being 2013 mentioned above.

Before 2013, housing and stock prices rose and fell together, highly correlated. After 2013, housing and stock prices were negatively correlated, although the fluctuations in A-shares were greater than those in housing prices.

The reason for the similar trends before 2013 is intuitive: when the economy was strong, corporate profits were good, especially for industries linked to the real estate cycle, such as building materials, home appliances, and landscaping. At this time, although interest rates were rising, corporate profits were expanding, so stock prices rose, and increased household income stimulated housing demand, leading to rising house prices.

After 2013, the entire market began borrowing new money to repay old debts, and real estate was no exception. The rising demand for real estate funds drove up interest rates. For stocks, especially A-shares dominated by traditional and cyclical industries, there was no significant improvement in profits during those years, and rising interest rates were a bearish factor for valuations. From a capital perspective, when rising house prices drove up interest rates, the returns on financial products became profitable, leading those with a high-risk appetite to buy houses and those with a low-risk appetite to purchase financial products, further differentiating the capital available for the stock market.

Most of the volatility in A-shares originates from capital conditions, which need to be viewed from the perspective of credit conditions. For example, the bull markets of 2006-2007 and the entire year of 2017 were characterized by credit easing, while monetary policy remained tight, driving interest rates higher.

The only exception was the bull market in 2015, which was characterized by loose money, with interest rates continuously falling, but credit remained tight, and the economy did not improve. A reasonable explanation is that due to several years of economic downturn, many underperforming businesses were passively eliminated from the market, while the continued easing of capital created a situation of "more water than fish," benefiting the surviving "fish" with benefits from leadership and monopolistic positions.

This is similar to recent years in Japan and Europe, where, despite population aging, weak demand, and stagnant economic growth, continuous monetary easing, combined with the continuous demise of businesses, has actually enhanced the competitiveness of large enterprises, optimizing their survival space and continuously increasing their profits.

From this perspective, we believe that real estate and A-shares will still experience a squeezing effect in the future, based on predictions of future interest rates and credit conditions: we are currently optimistic about A-shares and believe that the bull market in A-shares will last longer than expected.

There are three main reasons for this:

-

Interest rates in China are expected to decline slowly over the next five to ten years. Local debt swaps and financial support for the real sector require a long-term low interest rate environment. However, the decline in interest rates will not be as rapid as in the past in Europe and America and may even be lower than market expectations because China still needs to attract foreign capital with appropriate interest rates.

At least since 2013, industries that have consistently been booming, such as the internet, smartphones, the sharing economy, big data, gaming, and film and television, have relied on foreign capital's keen eye, technology transfer from developed countries, and global cooperation in their early stages, and the future will be no different;

-

Over the next five to ten years, domestic investment and financing expansion will rely more on the securities market. As mentioned earlier, due to high interest rates, even if they decline slowly, relying too much on credit will still follow the path of rising real estate prices because bank mortgages require collateral and reliable personal mortgage loans.

However, the valuation of the securities market is definitely based on the discounted future value. Therefore, recent reforms in the domestic capital market regarding listing, reduction, acquisition, and refinancing have been significantly liberalized. The state hopes that A-shares will become a paradise for adventurers in the future, hoping that these people will obtain and use enough money, hoping that the next Tencent or Alibaba will grow up in A-shares;

-

Over the next five to ten years, the global pattern of low interest rates, low growth, and high financing will not change, with cities' finances increasingly relying on local population consumption and corporate taxation, and investment and financing entities increasingly relying on businesses. Therefore, local governments will focus more on education, healthcare, entertainment, and other services. These expenditures were previously supported by land sales, a one-time transaction, but in the future, they are likely to rely on secondary charges from real estate, possibly property taxes or transaction value-added taxes.

Therefore, we are optimistic about the appreciation and dividends of high-quality stocks in the future, followed by the appreciation of high-quality residential properties and the rental income from low-priced commercial and residential properties, with bank financial products being the least attractive.

We believe that over the next five to ten years, India and Africa will not bring about a global economic recovery and overheating, and industries such as space and more efficient energy sources will not mature, so there is no need to worry about the low interest rate, low growth pattern being disrupted. Even if it is disrupted, it would be a fortunate event because by the time the economy overheats, assets will have appreciated significantly.

In summary, we advise readers with mortgages to switch to LPR (Loan Prime Rate) by mid-year and encourage entering the A-share market, increasing holdings, and actively participating in the upcoming bounty of new stocks and convertible bonds.

Additional note: This article was drafted on March 13, 2020 , and published on March 24. In the 10 days since, the overseas financial and economic environment has undergone tremendous changes. Optimists believe this crisis is a rerun of 1987, while pessimists think it's a repeat of 2008 or even 1929. In the context of globalization, no economy can remain unaffected. Before the pandemic subsides, global stock markets (including A-shares) will experience severe volatility. In a recessionary environment, only cash is safe. Now, keep your cash safe and prepare for future opportunities to purchase stocks and residential properties at significantly lower prices.