Basically, most of the dead P2P platforms or asset management products we see in our daily lives are Ponzi schemes.

Construct the Model of a Simple Ponzi Scheme

Generally speaking, there are only two kinds of participants in a Ponzi scheme: promoters who attract capital by promising incredibly high profits; and investors who pay money for above-average profits. Eventually, the promoters will run away when the funds are not enough to pay back every investor.

To simplify explanations, we assume that in a micro-society, a promoter has initiated a Ponzi scheme. The scheme will not be forced to stop due to the lack of regulators. It will only collapse when the promoter can no longer pay back the existing investors.

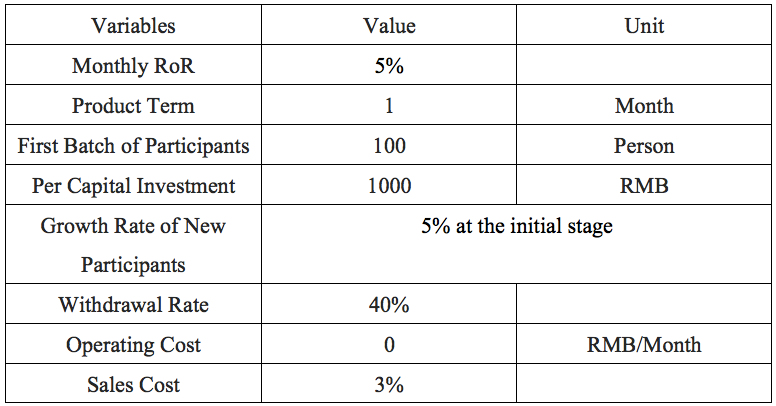

Assuming that the rules of the project and the initial conditions of each party are as follows:

Promoter's Intention

They attract more funds in order to extend the life cycle of the Ponzi scheme and gain enough time to skip town.

- Only use the funds from the new investors to pay back the existing investors,

- There is no monthly operating cost (such as labor and site costs) at all, while the comprehensive sales cost accounts for 3% of the scale of products in each term.

Investment Target

The funding game designed by the promoter to attract investors.

- The term for the product is one month, with a monthly RoR of 5%; investors can only reinvest or withdraw their money at maturity,

- When the product matures every month, the withdrawal rate is 40%; those who choose not to withdraw will reinvest,

- There is only one product during each term.

Investors

Participate in the scheme for higher profits.

- The per capita investment is 1,000 RMB,

- There are 100 investors initially,

- The monthly growth rate of participants is 5%.

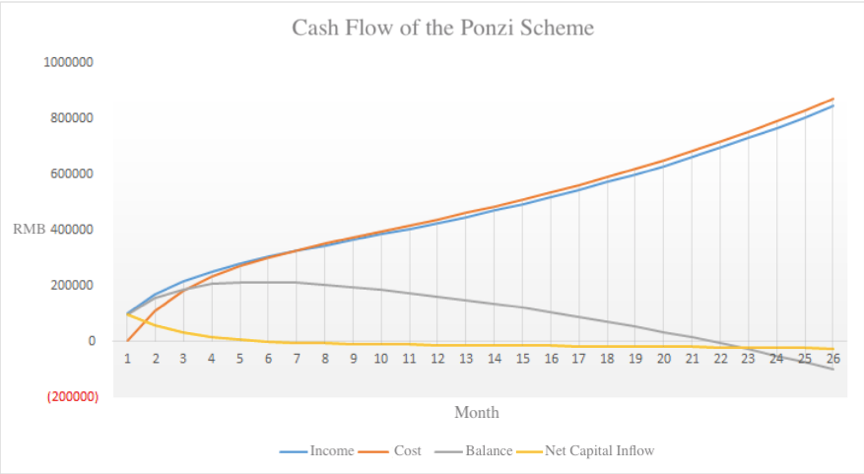

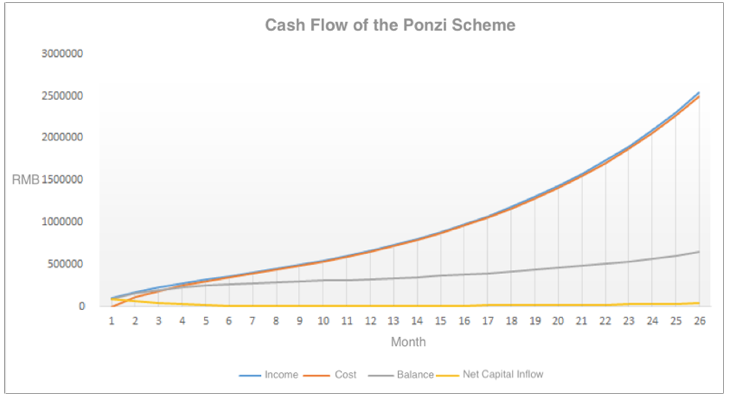

Accordingly, we can identify the key equations for calculating the income and cost in this experiment:

Current Income

= Funds from new participants in the current period + Reinvested funds from the prior period

= The number of new participants * Per capital investment + Total funds from the prior period * (1 - Withdrawal Rate)

Current Cost

= money paid to the existing investors in the current period + operating cost + sales cost

= Prior-period income * (1+ Monthly RoR) + Operating Cost + Current income * Sales cost rate

Net Capital Inflow

= Current Income - Current cost

Balance

= the sum of each period's net capital inflow

We can see that in the 22nd month, the balance of the promoter will be reduced to 0. In other words, the promoter is no longer able to pay back the investors. Therefore, the Ponzi scheme will last for up to 22 months.

However, given that the balance of funds reaches its peak in the fifth month, a rational promoter tends to skip town at this moment to maximize his or her own revenue, which is 213,759 RMB in this case.

Impacts of Different Variables

With reference to the basic model constructed in Part 1:

We have just assumed that there are two main purposes for Ponzi projects:

- Extend the life cycle of the scheme;

- Have a higher balance.

Next, let's take a look at the impacts of different variables on these two factors.

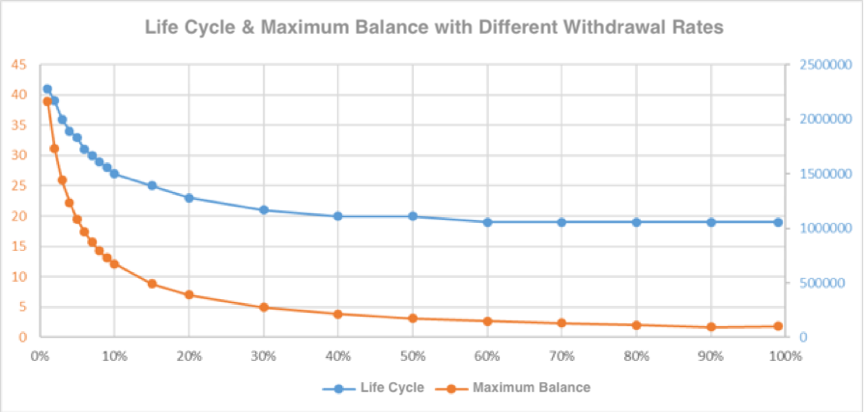

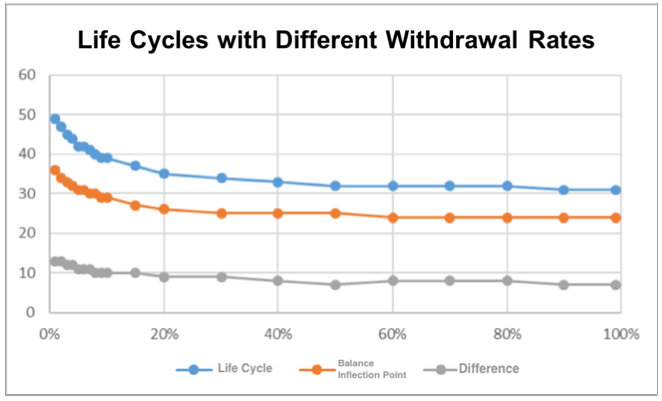

Impact of Withdrawal Rate

Suppose that other conditions remain unchanged, set the withdrawal rate from 1% to 99% respectively to calculate the life cycle and balance of the scheme.

We can deduce from the chart that for a scheme project, minimizing user's withdrawal rate can significantly alleviate its cash flow pressure, extend the life cycle and gain maximum profits.

Impact of Rate of Return, User Growth Rate, and Sales Cost

Higher rate of return (RoR) means an exponential increase of interest the project needs to pay back.

However, the Ponzi scheme is a game of "borrowing from newcomers to pay old users".

No matter how high the promised RoR is, fraudsters can always fulfil it as long as the growth rate of new users keeps up. In most cases, a higher RoR is more attractive to users. But it is worth noting that when frequent financial scandals are exposed in traditional markets, and the RoR of a project exceeds a certain threshold, it may adversely raise suspicion, leading to the decline in the user growth rate.

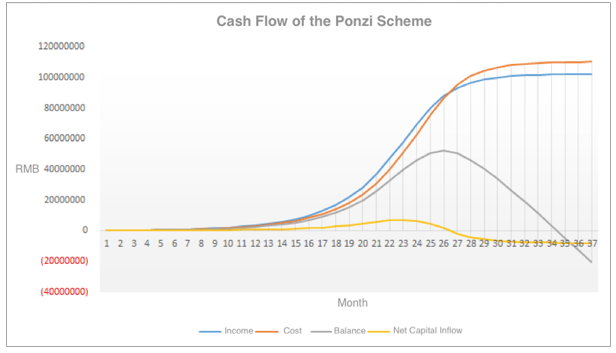

In our initial hypothesis, if there is no cap on the number of users, such model can run constantly simply by setting the user growth rate of each round at 10% as shown in the following figure.

If there is no limit to user growth rate, then in calculating the number of participants in an exponential function, we can see that even there are only 100 participants at the initial stage; growing at a rate of 10% after 166 months, the total participants can exceed 7 billion.

This is obviously impossible.

Surely, in the real world, when the number of participants reaches a certain scale, it will inevitably be constrained by factors such as geography, population, and culture, cutting off the sustainable growth of users. See, a ceiling exists.

Impact of Ceiling

Still, assume that there are 100 initial participants but increase the growth rate to 30% per period. When the number of newcomers reaches 20,000 in a certain period, the growth rate will stagnate and start to decline by 5% per month until it reaches zero.

Let's take a look at the changes in cash flow ceteris paribus.

When the user growth reaches a ceiling and starts to decline, the growth of net inflows drops sharply right the next month, and the balance soon turns to zero.

So, a ceiling can greatly restrict the scaling of the Ponzi scheme.

To study further, we can see that the withdrawal rate and rate of return have little effect on the life cycle when users grow at a high rate. Yet, once the participants reach a ceiling, the lower withdrawal rate can buy more time for the scheme.

Similarly, toggle the withdrawal rate from 1% to 100% and look at the life cycle and balance inflection point (from which the project will begin to make ends meet by using the former balances to cover interest). We find that after the withdrawal rate is decreased to 20%, both life cycle and the difference of balance inflection points are increased from 9 months to 13 months.

When a Ponzi scheme reaches the balance inflection point, a lower withdrawal rate can help buy more time for the project.

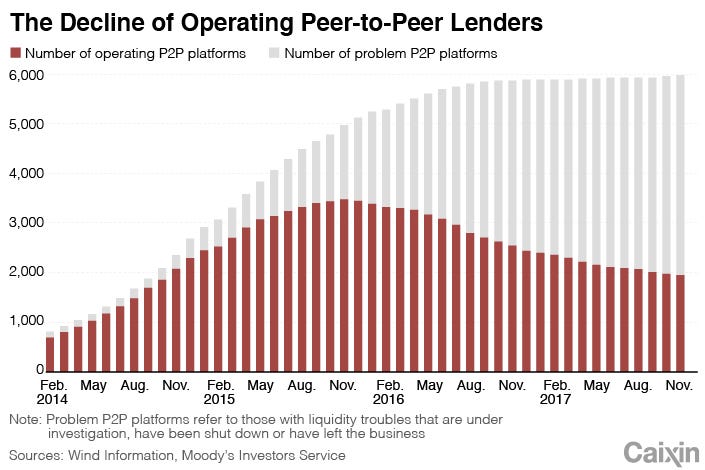

Case Study: Ezubao

Ezubao, a peer-to-peer lender, is founded in February 2014 and based in China's Anhui province.

Ceiling

In 2015, the estimated turnover of nationwide P2P platforms was less than 1000 billion with an average monthly turnover at 100 billion. Assuming that its users can expand nationwide without geographic restrictions, and eventually occupy 10% of market share; it can gain a maximum monthly income of 10 billion RMB.

Cash Outflow

The average annualized rate of turn of Ezubao is 12% with a monthly RoR of 1%; the monthly commission is calculated at an average of 0.5%; and assume conservatively that there are miscellaneous costs accounting for 20% of monthly total income (i.e. labour costs, workspace rental, registration fee of multiple shell companies, posting pictures of luxury cars pretending to be rich to attract new investors, as well as internal peculation).

Therefore, its monthly cash inflow needs to grow steadily at a rate of 21.5% or more to survive. (Ps. the turnover amount here includes the re-investment amount.)

Judging from this, when the monthly turnover exceeds 10 billion or the monthly growth rate is lower than 21.5%, it is highly possible that the Ezubao scheme will collapse.

Looking from the actual data, Ezubao's turnover in September 2015 already exceeded 10 billion (reached 13.45 billion). Turnover was 16.211 billion and 16.232 billion for October and November, growing by 20.5% and 0.1% respectively. The probability of Ezubao going bankrupt has increased greatly since October and the actual "detonation" time was right on December 3, 2015.

Conclusion

Though such a model is just an estimate, it is possible to predicate when a Ponzi scheme will collapse by estimating the ceiling and monthly cost.

1. There is a ceiling in the Ponzi scheme, which is definitely impossible to grow constantly

The ceiling of the Ponzi scheme varies according to investment markets, the education background of investors and financial openness. However, once the scale reaches a certain threshold, the scheme can collapse. This is why P2P giants like Ezubao and Fanya can grow rapidly in the early stage but soon fail after reaching turnovers of billions.

2. Team's execution capability determines whether the ceiling can be reached

Although the Ponzi scheme does have a ceiling, it cannot be used to judge when the fraud team will run away. If the team lacks execution ability or ambition, the scheme can go bankrupt and the team can run away even without reaching the so-called ceiling.

3. The only choice is to grow exponentially, fission or multi-level distribution is just essentially inevitable "expediency"

Since the cost of interest is exponentially growing, the growth of new users must keep up with it in order to maintain the operation. When the number of users reaches a certain scale, it is difficult for the team to reach out to sufficient users using its own capability, so it turns to market by word of mouth or viral advertising. Therefore, means like fission and multi-level pyramid schemes may be the only effective options to grow exponentially in the short term.

4. Be wary of a slowdown in growth, and watch out for the sudden drop in the withdrawal rate

The growth rate is the only lifeline of a Ponzi scheme.

When the growth rate starts to slow down or even decline, it is time for investors to be cautious. The team will usually take the following actions to cope with the panic withdrawal:

a. Reduce the withdrawal rate through coercive means like lengthening the verification period and controlling public opinions;

b. Exaggerate the profits and raise the user's withdrawal cost, e.g. suddenly increasing the rate of return in the short run, or increasing profits through a longer lock-up period;

c. Develop various tools or games on the platform to keep users' money.

Remember, such behaviors can only buy some time for the team in the short term. Stay cautious when you see such signals.

5. When the net inflow is negative, the possibility of the team running away increases

In the traditional industry, it is difficult for us to collect information about the company. However, in the blockchain field, since all data can be reviewed on the chain, the funding situation is transparent. Many Ponzi schemes need to use a public wallet address as the depositing channel. If you know its wallet address, you may have the chance to find out when the team runs away.

The Ponzi scheme dates back to 1919, and the Madoff's $65-billion-fraud gave birth to more complex patterns. In the crypto front, models like ideological stamp, gravitational lens, and the likes are just using these conceptual names to talk big, which casts a shadow over many science fiction terms.

No matter how the model changes, the most important thing is to keep a clear mind and grasp the essence of things quickly. These findings are not only relatable to the Ponzi schemes, but also for daily life.